In the parcel delivery industry, driver shortages and complex relationships with transport subcontractors are critical challenges. Unfortunately, subcontractor bankruptcies have become all too common, often due to the difficulty in accurately calculating their profitability and negotiating fair agreements with delivery companies.

In this article, we will delve into the issues faced by subcontractors, examining the underlying reasons behind their financial struggles, and offering solutions to improve their situation. To illustrate these challenges and solutions, we will also present a real-life case study.

Transport subcontractors at risk

The subcontractor model is widely adopted throughout the industry, with many relying heavily on subcontractors for their last mile operations (for example, 80% of parcel delivery platforms in Paris region subcontract it). This reliance on subcontractors brings forth a unique challenge – they represent the face of the company, especially for e-commerce clients. In many cases, they are the only individuals customers interact with during the delivery process. Thus, retaining skilled and dependable drivers becomes a monumental challenge. According to a Scandit research (2021), 37.8% of last-mile shipping companies in North America said that getting a qualified driver was the most significant challenge (32,4% in Europe).

In 2022, one of the largest postal parcel companies in the United States reported an astonishing 59% turnover rate. This figure means that at least half of their drivers either left the company. In 2019, this figure stood at 38.5%, which represents an increase of 20 percentage points in just 3 years! Such high turnover rates have profound implications for service quality and overall performance.

However, the financial well-being of subcontractors is highly vulnerable, primarily because they handle the last-mile delivery, which is both complex and costly. In fact, the last mile constitutes the largest portion of these costs, accounting for 53%, and stands as a crucial element in the overall cost structure.

In summary, the challenges facing transport subcontractors in the parcel delivery industry are multifaceted and demand innovative solutions to ensure both their sustainability and the quality of service they provide.

Last mile: what pricing for subcontractors?

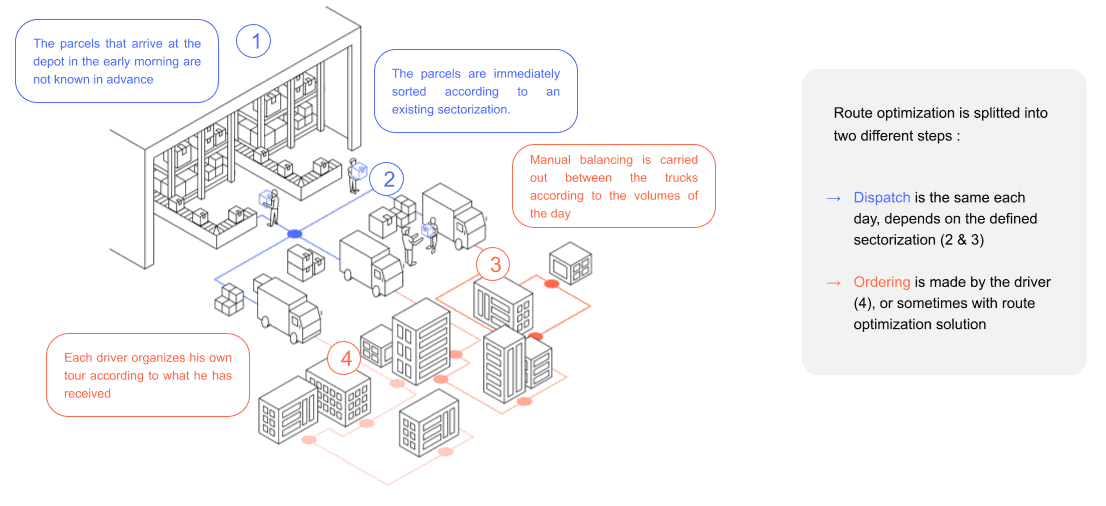

How is route optimization organized in the parcel delivery industry?

Before delving into the causes and solutions for the challenges we’ve identified, let’s take a closer look at the pricing model for subcontractors in the last-mile delivery process. In the last-mile depot, this process can be broken down into two key steps.

The first step is dispatch, which is typically managed by internal personnel from the parcel delivery company. They are responsible for organizing the sorting and dispatching of parcels. Sometimes, it may even be the drivers themselves who handle this step, depending on the company’s practices. However, it’s important to note that the dispatch process is usually predetermined in advance, often determined by contractual agreements**.**

When working with subcontractors, the common approach is to assign them specific areas defined by several zip codes. Their responsibility is to serve these designated zip codes comprehensively, meaning they must deliver all parcels within that area. It falls upon the subcontractor to make this happen efficiently.

It is the subcontractors who handle the second stage of the process: route scheduling. Typically, subcontractors tend to organize their operations so that each delivery driver has a designated area for which they are responsible. This approach allows for precise sorting within these smaller, driver-specific zones, rather than managing deliveries across the entire region. Subcontractors may need to balance the workload among drivers for a more equitable distribution of deliveries.

How subcontractors are compensated?

Subcontractors in the parcel delivery industry are typically compensated based on a pricing model, and one of the most common approaches is the price-per-parcel model.

In this model, subcontractors are assigned specific sets of zip codes within which they are responsible for making deliveries. They are then paid a fixed rate for each parcel they successfully deliver. While this model forms the basis, it can become more intricate in practice. Variations in compensation may arise based on factors such as the type of delivery, whether it’s deposited in a locker, sent to a pick-up and drop-off (PUDO) point, or delivered directly to an individual. Additionally, there may be penalties imposed for issues related to the quality of service, ensuring subcontractors are incentivized to maintain high standards.

However, for the sake of simplicity, let’s consider the standard price-per-parcel model. From the perspective of the parcel delivery company, this model offers predictability and control. It ensures that as parcel volumes increase or decrease, the associated costs rise or fall linearly, eliminating unexpected cost spikes that could arise from doubling or quadrupling volumes.

Yet, in practice, negotiating a uniform price-per-parcel can be challenging. Factors such as a specific geographic area or the subcontractor’s level of experience can complicate the establishment of a standard rate. One key factor contributing to this complexity is the scarcity of data. In some cases, determining an appropriate price-per-parcel can be a daunting task, as accurate data may be lacking.

Subcontractor pricing: what drives negotiation?

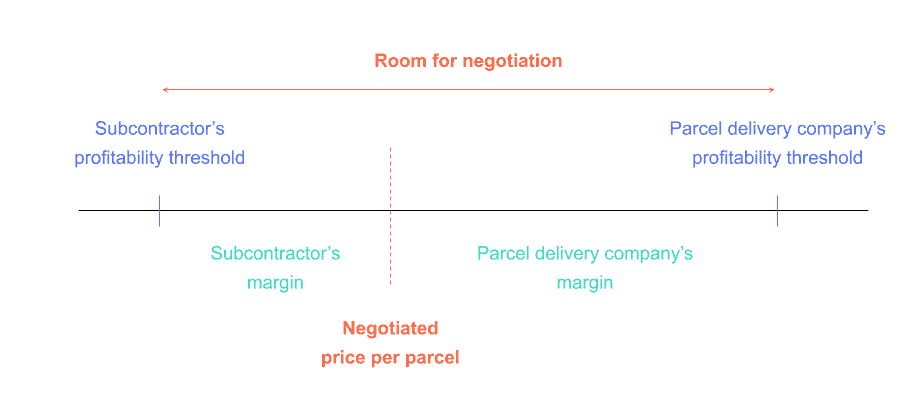

So, what is the key to finding a solution? It all comes down to striking the right balance in pricing, and this balance lies somewhere between two critical thresholds.

Firstly, there is the profitability threshold for subcontractors. When we delve into the cost structure of subcontractors, we discover that the majority of their costs fall into the category of fixed expenses. These include payments to their drivers and the upkeep of their trucks, whether they own or rent them. There’s also a variable cost component linked to energy expenses, which may slightly fluctuate based on the distance covered during deliveries. However, in the parcel delivery industry, variations in kilometers traveled are generally limited, and energy costs play a relatively minor role in the overall cost structure.

On the other hand, we have the parcel delivery companies themselves, which also incur substantial fixed costs. This is a key reason why many parcel delivery companies opt to rely on subcontractors for the last-mile delivery, as it allows them to maintain a highly variable cost structure. This variable cost structure is often implemented through the price-per-parcel model we discussed previously, enabling parcel delivery companies to keep a close watch on costs and enhance profitability.

The challenge is to find the sweet spot in between these two thresholds. It is important to note that this balance is not set in stone. In some cases, these thresholds might be reversed, especially when parcels have already been sold to a specific retailer. If this retailer is heavily concentrated in areas that are far from the depot, the price received for these parcels may be very low, and the subcontractor’s costs could exceed what can be feasibly spent on last-mile delivery. The room for negotiation can vary significantly based on factors like the structure and geography of the delivery area. In some situations, there may be very little room for negotiation, or it might not exist at all.

In our article, we will primarily focus on the subcontractor’s profitability threshold. Parcel delivery companies often have a good grasp of their cost structure, particularly for each parcel they transport through the entire logistics chain. However, subcontractors face greater challenges in accurately assessing their cost structures, especially when they are new to an area.

Real case study: deepdiving the subcontractor cost structure

Perimeter of the subcontractor’s activity

Let’s take a deep dive into a real case study to gain a better understanding of how subcontractor pricing is approached and why it can sometimes fall short or become counterproductive.

In this case, we will focus on the specifics of a particular subcontractor’s activities. The data represents the kind of information that the person responsible for negotiation had to work with.

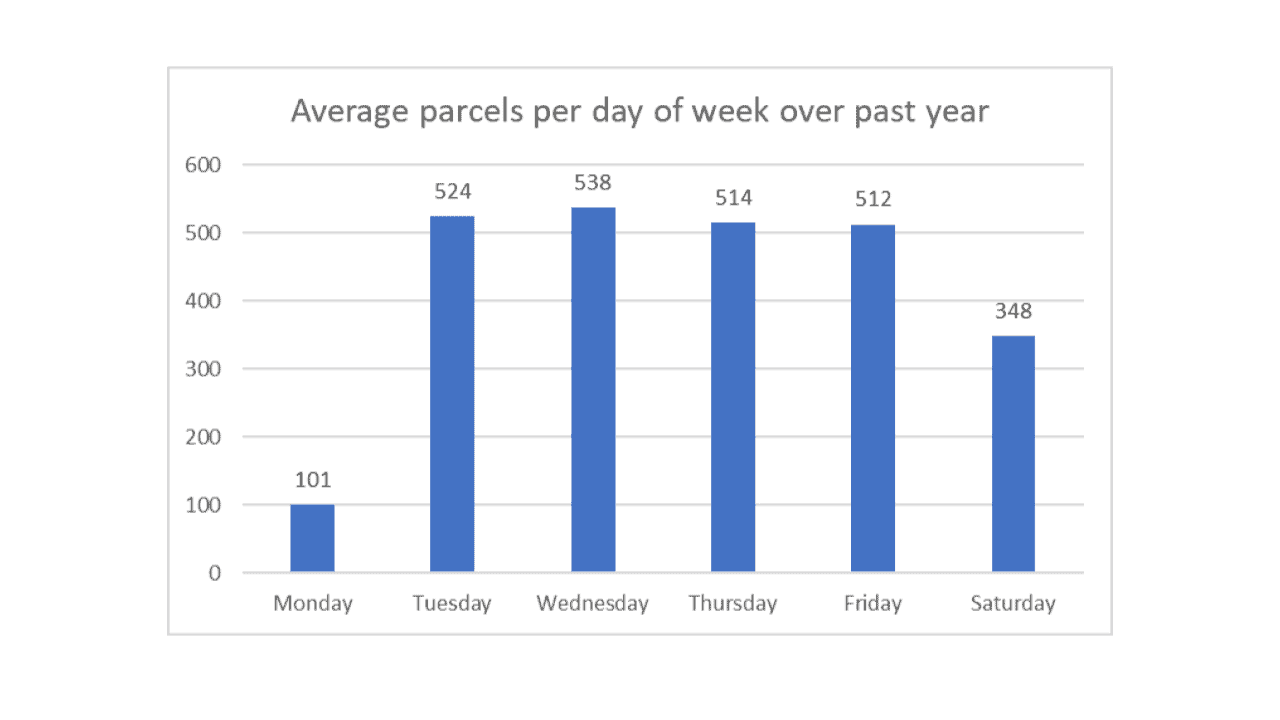

On the designated area for this subcontractor, they were handling an average of 460 parcels per day with the help of eight drivers. The average distance traveled by the vehicles was approximately 100 kilometers. Now, let’s break down the cost structure. There were identified fixed costs, which included leasing expenses for the vans and the salaries of the drivers. This fixed cost remains the same, regardless of how many parcels are delivered each day. For example, if only four drivers are needed on a particular day, you still have to pay for all eight drivers.

Additionally, there were variable costs, which amounted to around €10 per day for each actively used driver. These costs depended on factors such as the tools deployed in the field, as the vans consumed energy and incurred operational expenses.

The graph illustrates how the activity varied throughout the week, with Tuesdays and Wednesdays showing the highest volume of deliveries. This fluctuation allowed the subcontractor to strategically schedule days off for some drivers on Mondays and Saturdays to compensate for the busier days and ensure they could manage the weekly seasonality with the available eight drivers.

Based on this data, the team estimated the average delivery cost for the subcontractor per parcel at €1.79. To arrive at this figure, they considered factors like potential 5% increases in energy prices. They added a 5% margin to ensure a reasonable profit margin for the subcontractor, resulting in a negotiated price of €1.88 per parcel. It is important to note that without more detailed data, this was likely the best estimation they could achieve.

Analysis of the subcontractor’s activity

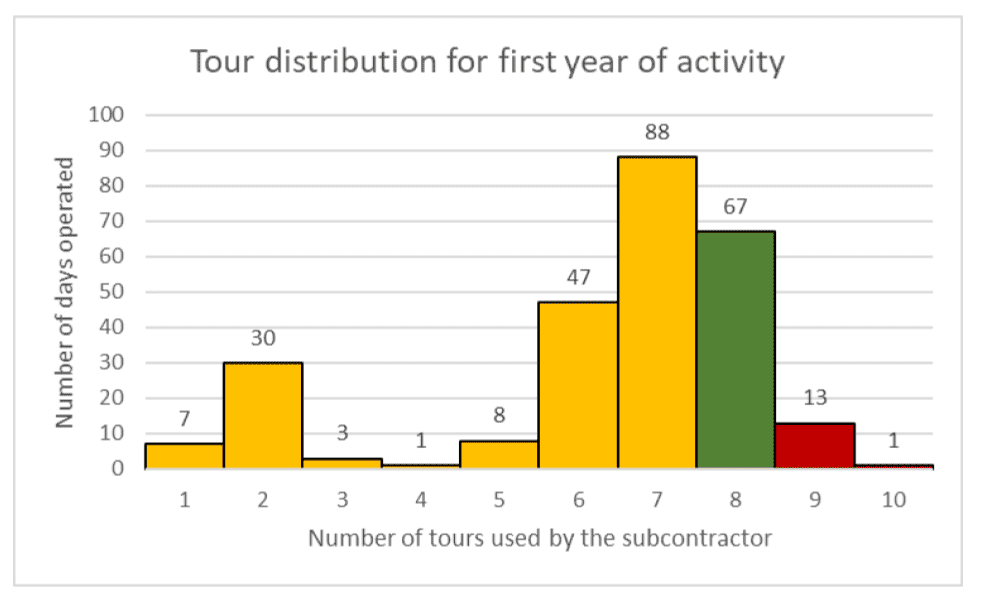

On the graph, you can see the results of simulations conducted to address these challenges. The use of 7 tours is the most common scenario. However, there are days when more than 8 tours may be required, especially during peak activity, and others when only 6 or even 5 tours are necessary.

The central question that arises is whether the utilization of eight tours is adequate or if it’s excessive. Determining the right level is crucial for ensuring the system’s efficiency and profitability. This challenge highlights the complexity of establishing an optimal compensation model for subcontractors that accommodates fluctuations in parcel volume and external factors like energy prices.

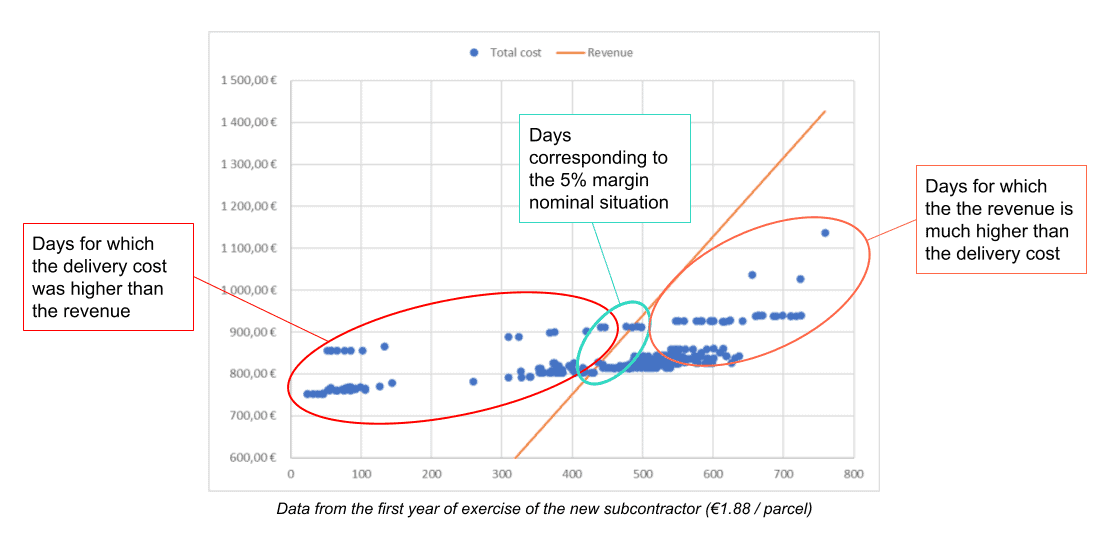

This graph provides valuable insights into the subcontractor’s performance over the course of a year, following the establishment of the €1.88 per parcel pricing.

On the X-axis, you can observe the number of parcels for each day, with each blue dot representing a past day of activity. For every day, we were able to meticulously calculate the number of parcels the subcontractor had to deliver and precisely compute their costs. This cost calculation took into account both fixed expenses and variable costs based on factors such as kilometers traveled.

The orange line on the graph represents revenue, and it forms a perfectly straight line due to the fixed pricing of €1.88 per parcel paid to the subcontractor.

However, what becomes evident is the significant disconnect between the subcontractor’s cost structure and their revenue. Many of the issues we’ve discussed throughout this article stem from this misalignment. The blue points can be located to the left or to the right of the orange line, indicating whether the revenues are lower or exceed the delivery costs.

The days that align with the 5% margin we initially identified and based our calculations on correspond to the nominal situation when the price was set at €1.88 per parcel. However, in practice, the variations are much more significant than the initially estimated 5% around the average. Setting the right price under these circumstances is incredibly challenging.

Depending on the time of year, the cost structure will not be the same. With the hiring of temporary drivers, the peak season increases it significantly. These insights highlight the intricacies of subcontractor compensation and the challenges of aligning pricing with varying cost structures and seasonal fluctuations.

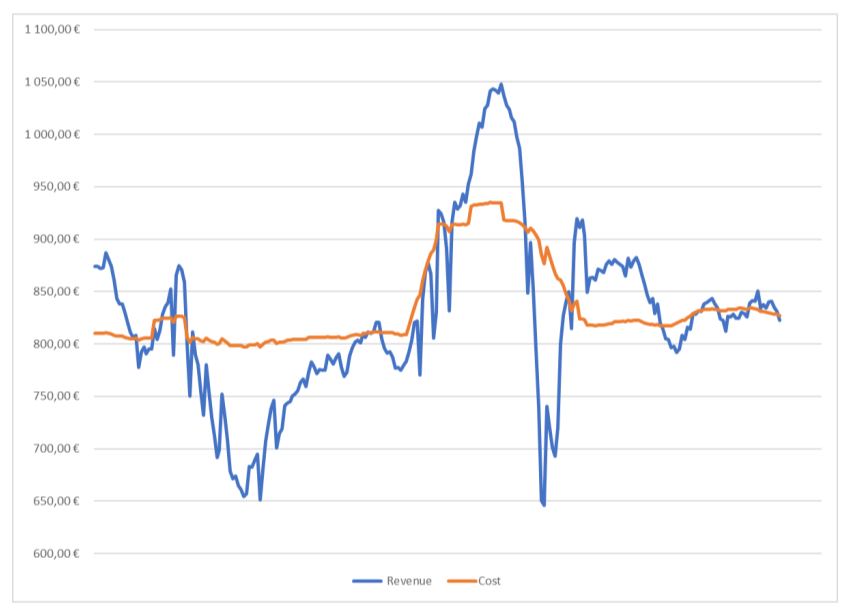

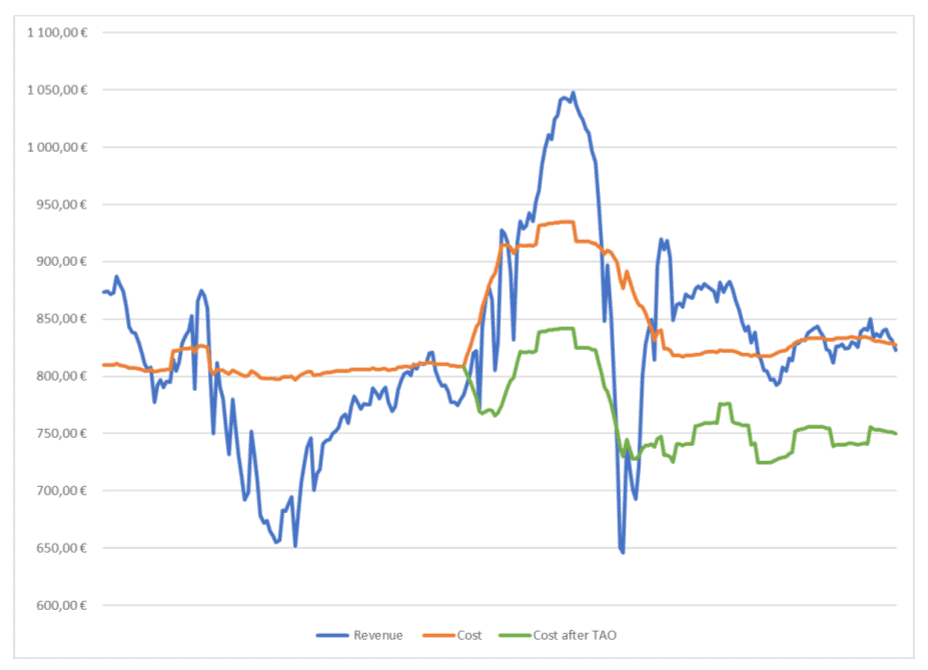

Let’s examine the situation from a different perspective, considering both revenue and costs over the course of a year, month by month. The graph below reveals data from June 2021 to April 2022.

We can observe significant revenue oscillations: a notable drop in August, followed by an increase in parcel volumes during the peak season, and then another drop in January before stabilizing. This variation is quite significant, almost doubling over the span of six months.

In contrast, the cost structure remains relatively stable. The subcontractor finds it challenging to adapt to such revenue fluctuations, as fixed expenses must be paid regardless.

The sudden increase in cost, marked here, corresponds to the additional driver recruited in October. It appears that the decision to hire this driver may have been made prematurely, as the cost structure increased more rapidly than the revenue during this period. This highlights the importance of anticipating and timing such decisions accurately.

So, at the end of this nearly full year of operation, it resulted in a loss of revenue (-€1,660.93), with a negative margin (-0,8%) even though we aimed for a 5% positive margin. Such a situation can be highly critical for a subcontractor on the brink of bankruptcy. Understanding these dynamics and forecasting business performance and profitability one year in advance is extremely challenging.

Kardinal's approach to ensure collaboration’s profitability

So, what can be done to address this challenge? There are several approaches, but a smarter strategy is needed to maintain profitability for parcel delivery companies while compensating subcontractors fairly. Keep in mind that our suggestions are not exhaustive, but they contribute to tackling this issue.

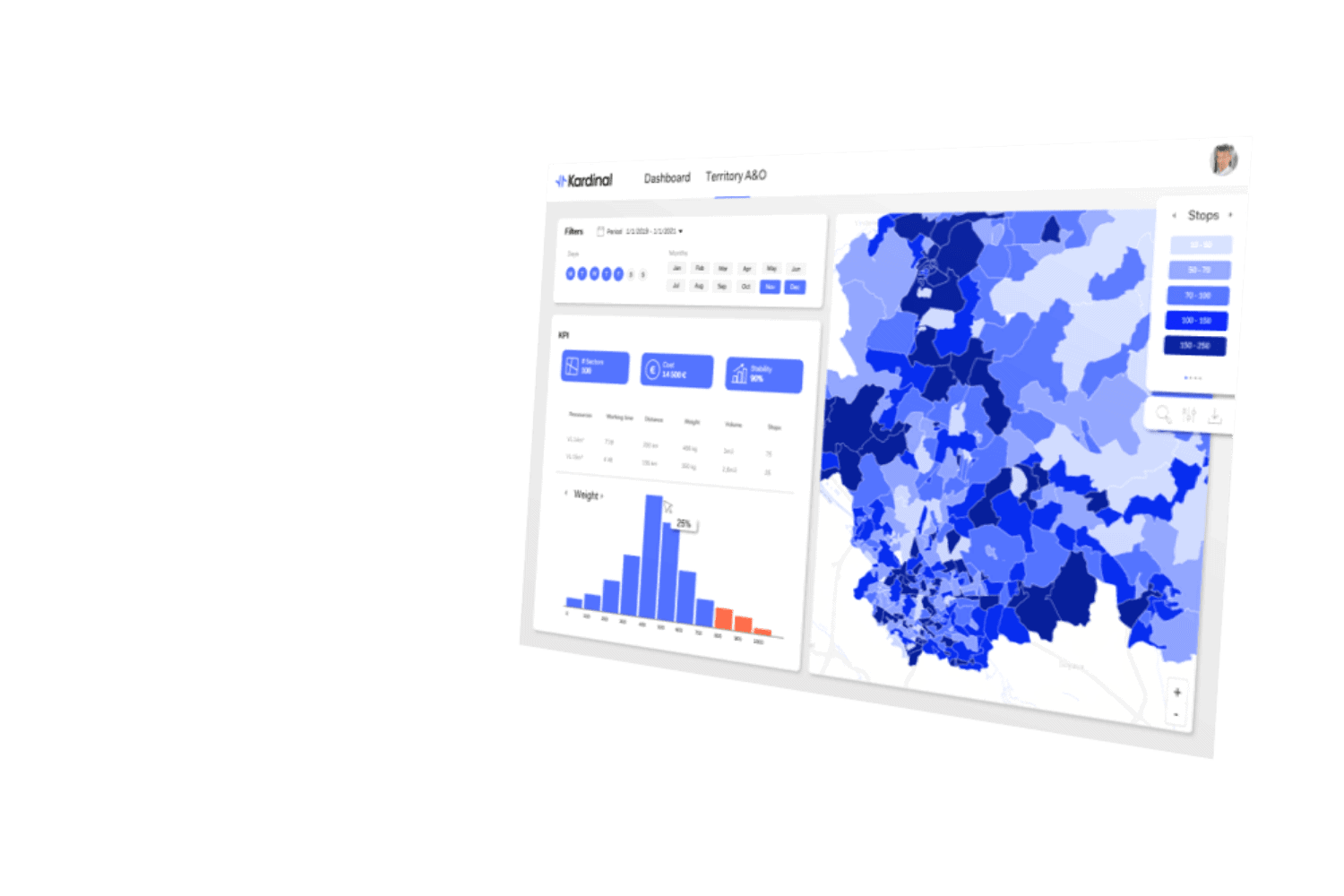

Kardinal has developed “Territory Analytics & Optimization (TAO)” solution focused on tactical and strategic decision support, specifically sectorization optimization. This tool helps split territories into sectors for subcontractors, facilitating price negotiations.

1- Building in-depth understanding of the structural delivery cost of a subcontractor’s area

Our first recommendation is to gain a deeper understanding of the structural delivery costs in a given area. Often, subcontractor pricing is based on previous rates or benchmark prices, which may not be optimal. Subcontractor turnover should be viewed as an opportunity to reoptimize and create a more cost-effective arrangement.

Understanding the delivery cost structure is crucial. Areas far from the depot with low density naturally require higher prices due to lower productivity. Estimating the true cost through simulations ensures that subcontractors can work with the proposed prices while also ensuring the lowest possible cost for the delivery company.

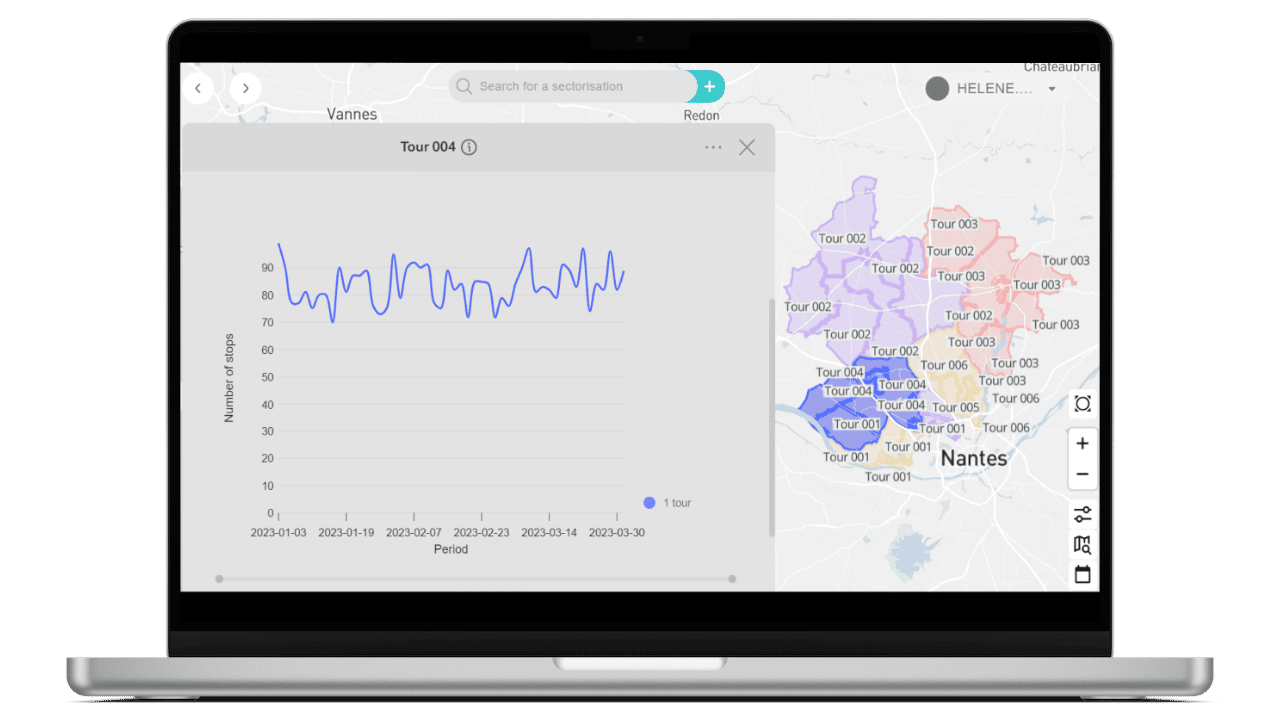

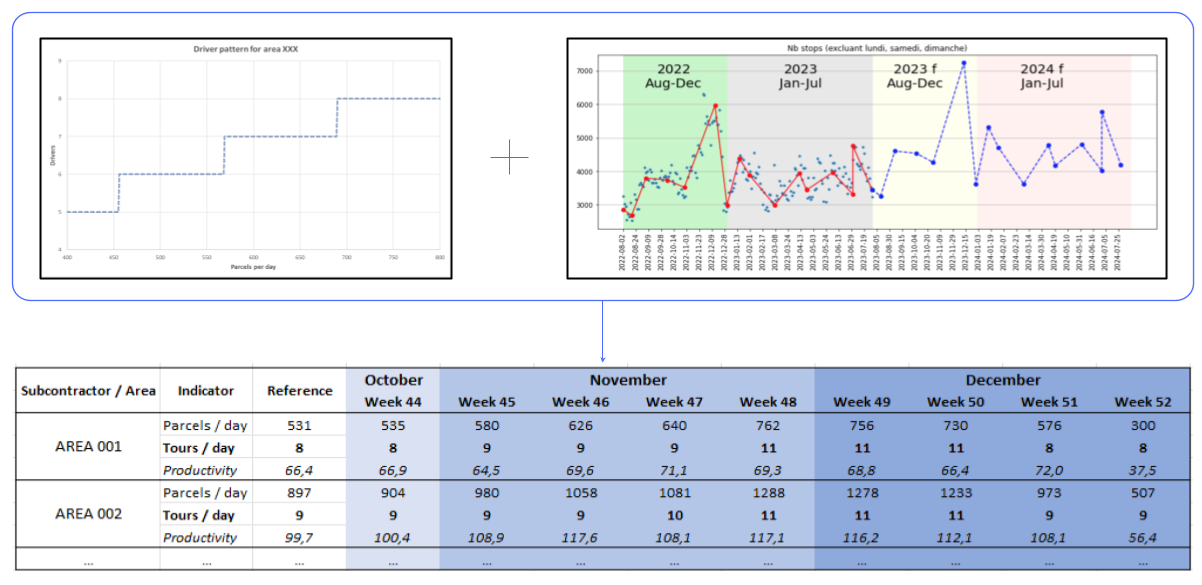

For example, consider a scenario where a subcontractor manages 6 routes. The tool allows users to specify a timeframe, including days of the week, and months. Using this data, accurate estimates can be provided for each of these routes, including the average number of kilometers traveled, the required number of drivers, and their working hours.

What enhances the Kardinal solution’s value is its capacity to offer insights into variations. Users can observe how these metrics change over time, such as the average weekly kilometers traveled. This thorough examination of the data facilitates a comprehensive understanding of the subcontractor’s cost structure, which is vital for determining appropriate pricing.

2- Predicting activity level to help subcontractors anticipate their recruitment

One of the major challenges for a subcontractor is anticipating their resources, especially during the peak period. To address this, we have implemented an initiative for some of our clients, which involves anticipating this intense period by combining Machine Learning forecasting technologies, based on recent trends and data from the previous year. We create various scenarios to determine how this peak season will unfold in each specific region for a subcontractor.

We use these scenarios to estimate the delivery model, determining, for example, how many parcels will be delivered each day in a given region and how many drivers will be required. For some of our clients, we provide a detailed week-by-week plan, taking into account each subcontractor’s workload.

What you see here is an anonymized illustration of real data. For example, in the first area, we estimated that the reference would be approximately 531 parcels per day at the beginning of the peak season. We then projected how this workload would evolve during the period and how many drivers would be needed each week to maintain operational stability.

This approach is crucial because subcontractors often lack visibility during this peak period. They may react too early by hiring too many drivers in advance, resulting in financial losses, or react too late, affecting service quality. By providing increased visibility and clear recommendations to subcontractors, we help them plan rather than react, which is essential for managing their cost structure, including fixed costs.

3- Reorganize territory so subcontractors are big enough to reach the critical mass of 10 drivers

For some players in the parcel delivery industry, subcontracting the last mile to transportation partners with a sufficient number of drivers is a good practice to manage fluctuations. A subcontractor employing at least 10 drivers has more flexibility in organizing their routes. The higher the number of drivers, the more stable the cost structure and performance. The optimization potential with a tool like Kardinal is also greater. Thus, by encouraging subcontractors to grow with you, you engage in a real collaboration with them.

However, there are other ways, including ensuring they work as a team. If two subcontractors with five drivers each work together as a team, as if they were one, it can also be a good option if they can effectively organize together.

As we have seen, implementing this type of policy yields very good operational results for clients. It makes everything much easier, provided that the subcontractor is well supported.

Kardinal optimization results

Let’s revisit the previously presented case study. Thanks to Kardinal’s TAO solution, the subcontractor was able to optimize its operations. By using forecasting capabilities to anticipate the peak period and further optimize the cost structure, we managed to remove one route starting from late September. The recruitment of an additional driver to support peak activity was also delayed by a few weeks.

Despite the volume decline in 2022 due to inflation, the subcontractor was profitable every month. In the end, over this period, they saw an increase in their revenue (-€1,660.93 without optimization versus +€11,265.05 with Kardinal) and their margin (-0.8% without optimization versus +5.4% with Kardinal).

In conclusion, the parcel delivery industry is facing significant challenges related to driver shortages and complex relationships with subcontractors. High driver turnover rates directly impact service quality, while the financial health of subcontractors is often precarious due to the complexity and high costs associated with last-mile delivery.

The pricing of subcontractors is a crucial aspect of this dynamic. Striking the right balance between subcontractor profitability and the financial viability of parcel delivery companies is a complex challenge. Fixed and variable costs, as well as seasonal fluctuations, make standard pricing difficult to establish.

Kardinal’s approach, grounded in a deep understanding of structural costs, activity forecasting to anticipate workforce needs, and territory reorganization, provides solutions to ensure the profitability of collaboration between subcontractors and parcel delivery companies.

Ultimately, these solutions enable the creation of more equitable and sustainable relationships among industry stakeholders while maintaining the quality of service provided to customers.